Introduction: Building Dreams, Protecting Investments in California

California homeowners embark on projects big and small – from a stunning ADU addition to a modern kitchen remodel, a resilient new roof, or a sustainable solar energy system. Each endeavor represents a significant investment, a vision for improved living, and a step towards enhancing your property's value. Yet, amidst the excitement of transformation, many homeowners overlook one of the most critical aspects of hiring a contractor: their insurance coverage.

In the Golden State, where property values are high and regulations are stringent, the question isn't just "Does my contractor have a license?" but "Are they adequately insured?" Uninsured or underinsured contractors pose hidden risks that can turn your dream project into a financial and legal nightmare. This comprehensive guide from Powercore Inc, your trusted dual-licensed General B & C-10 Electrical Contractor, will demystify California contractor insurance requirements, empowering you to make informed decisions and safeguard your most valuable asset: your home.

Why Contractor Insurance Isn't Just a "Requirement" – It's Your California Shield

For many, contractor insurance sounds like a dry, bureaucratic detail. In reality, it's the financial bedrock that protects you, your property, and your peace of mind throughout any home improvement project. In a state like California, with its bustling construction industry, diverse terrains, and high cost of living, the stakes are exceptionally high. Here's why robust contractor insurance is your indispensable shield:

- Protecting Your Assets: Your home is likely your largest investment. Should an accident occur – a fire, structural damage, or a major plumbing leak – adequate insurance ensures that the financial burden doesn't fall squarely on your shoulders.

- Mitigating Liability: If a worker is injured on your property, or if a third party (like a neighbor) incurs damage due to the contractor's work, without proper insurance, you could be held personally liable. This could mean devastating legal fees, medical costs, and potential loss of assets.

- Ensuring Project Completion & Quality: While not direct insurance, bonds (often associated with insurance) provide a layer of protection if a contractor abandons a project or fails to meet contractual obligations.

- Peace of Mind: Knowing your contractor is fully insured allows you to focus on the exciting aspects of your project, rather than worrying about potential catastrophes.

Choosing a fully insured contractor isn't just about compliance; it's about intelligent risk management for the discerning California homeowner.

Key Types of Insurance Every California Contractor Needs (and Why They Matter to YOU)

Understanding the different types of insurance your contractor should carry is crucial. Each serves a distinct purpose, collectively building a robust safety net for your project.

General Liability Insurance: Your Home's First Line of Defense

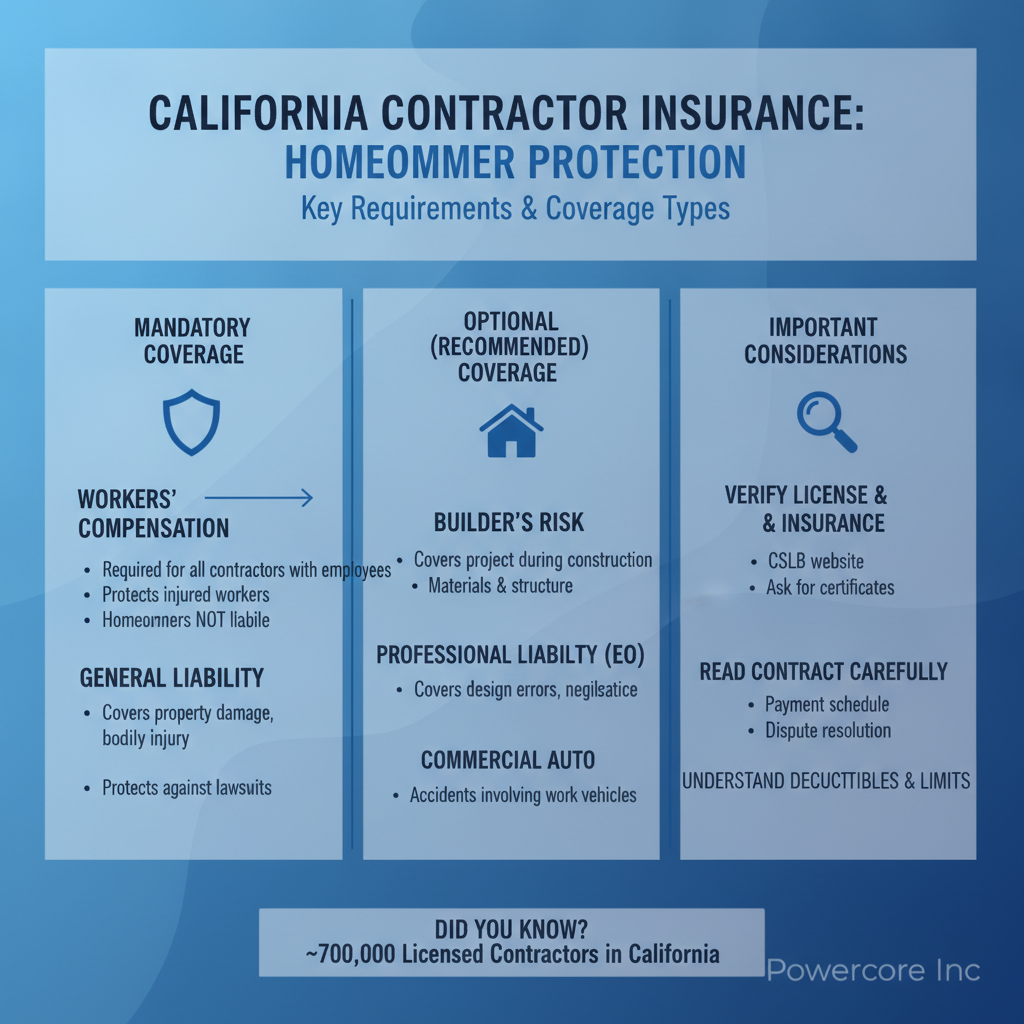

This is arguably the most critical insurance for any contractor. General Liability (GL) insurance protects against claims of bodily injury or property damage that occur during the course of the contractor's work or as a result of their operations.

- What it Covers:

- Damage to your existing property (e.g., a worker accidentally drops a tool, causing a hole in your wall or breaking a window).

- Injury to a non-employee (e.g., a delivery person or neighbor trips over equipment left on your property).

- Damage to a neighbor's property caused by construction activities.

- California Context: While California does not legally mandate General Liability insurance for all licensed contractors, the California Contractors State License Board (CSLB) strongly recommends it. Reputable contractors like Powercore Inc will always carry substantial GL coverage, often $1 million per occurrence or more, reflecting their commitment to client protection.

- Why it Matters to You: Without GL insurance, you, the homeowner, could be directly responsible for repair costs or medical bills stemming from accidents related to the work being done on your property. This could lead to costly litigation and significant out-of-pocket expenses.

Workers' Compensation Insurance: Protecting Those Who Build Your Dreams

If a contractor has even one employee, California law mandates they carry Workers' Compensation (WC) insurance. This is a non-negotiable requirement for the safety of both the workers and the homeowner.

- What it Covers:

- Medical expenses for employees injured on the job.

- Lost wages for employees unable to work due to a job-related injury.

- Rehabilitation costs.

- California Context: The CSLB rigorously enforces Workers' Comp requirements. A contractor's license can be suspended or revoked if they fail to maintain this coverage while employing workers. The CSLB website will indicate if a contractor carries Workers' Comp.

- Why it Matters to You: If an uninsured worker is injured on your property, you, the homeowner, could be deemed the "employer" and held responsible for their medical bills, lost wages, and potentially face lawsuits. This scenario can quickly escalate into a financial catastrophe, easily running into hundreds of thousands of dollars. Always verify Workers' Comp if your contractor has a crew.

Contractor's Bond (Surety Bond): A Promise of Performance

While not technically insurance, a contractor's bond is a critical financial guarantee required by the CSLB and offers vital protection to consumers.

- What it Covers: A contractor's bond ensures that the contractor will comply with state licensing laws and contractual obligations. If a contractor fails to complete a project, violates CSLB rules, or causes financial harm, the bond can be used to compensate the affected party.

- California Context: All licensed contractors in California (including Powercore Inc, with General B #1134334 and C-10 Electrical #1098175) must maintain a $15,000 contractor's bond with the CSLB. Additionally, contractors undertaking home improvement projects over $5000 may need to obtain a separate "Contractor's Performance Bond" or "Payment Bond" depending on the project scope and client preference, offering an even higher level of protection.

- Why it Matters to You: The bond provides an avenue for recourse if your contractor fails to perform as agreed, offering a layer of financial protection beyond just their insurance.

Commercial Auto Insurance: On the Road and On Your Property

Contractors use vehicles daily to transport tools, materials, and personnel. Commercial auto insurance protects against accidents involving these work vehicles.

- What it Covers: Bodily injury and property damage resulting from accidents involving company-owned vehicles.

- Why it Matters to You: If a contractor's vehicle damages your property (e.g., drives onto your lawn, hits a fence) or causes an accident on or near your premises, their commercial auto insurance covers the damages, preventing you from becoming embroiled in liability claims.

Builder's Risk (Course of Construction) Insurance: For Major Transformations

For larger projects like ADU construction, extensive home remodels, or new builds, builder's risk insurance is a specialized policy that covers the structure and materials during the construction phase.

- What it Covers: Damage to the building and materials from perils such as fire, theft, vandalism, storms, and other natural disasters during construction.

- Why it Matters to You: Your standard homeowner's insurance policy often has limitations or exclusions for properties under construction. Builder's Risk ensures that your significant investment in the project itself is protected from unforeseen catastrophic events before the project is completed and your regular homeowner's policy can fully resume coverage. It avoids disputes over who is responsible for damage to the partially completed structure.

California's Regulatory Landscape: What the CSLB Mandates

California has one of the most robust contractor licensing boards in the nation: the Contractors State License Board (CSLB). The CSLB sets strict standards to protect consumers and maintain professionalism within the construction industry.

- Licensing Requirements: Any individual or company that contracts to perform construction work in California that costs $500 or more (labor and materials) must be licensed by the CSLB. This includes all services offered by Powercore Inc, from solar and battery storage to HVAC, EV charging, and siding.

- Bonding: As mentioned, every licensed contractor must maintain a $15,000 contractor's bond. This bond is specifically designed to protect consumers from financial losses if a contractor violates the law or breaches a contract.

- Workers' Compensation: If a contractor employs even one person, they are legally required to carry Workers' Compensation insurance. The CSLB actively monitors this and will not issue or renew a license without proof of coverage or a valid exemption.

- Powercore Inc's Commitment: As a California dual-licensed General B (#1134334) and C-10 Electrical Contractor (#1098175), Powercore Inc not only meets but exceeds these stringent requirements. Our licenses signify our adherence to the highest standards of financial responsibility, technical expertise, and consumer protection mandated by the state. This comprehensive licensing allows us to handle a vast array of projects, ensuring seamless integration and accountability across all trades.

The Perils of Uninsured Contractors: A California Homeowner's Nightmare

The allure of a cheaper bid from an uninsured contractor can be tempting, but the potential consequences far outweigh any upfront savings. Engaging an uninsured contractor in California is a gamble with your finances, your property, and your peace of mind.

- Direct Financial Liability: If an uninsured worker is injured on your property, you could be held personally liable for their medical expenses, lost wages, and even long-term disability. California's legal system is designed to protect workers, and without Workers' Comp, the burden often shifts to the homeowner. This isn't just a theoretical risk; it's a real and devastating possibility.

- Property Damage Costs: Should an uninsured contractor or their crew damage your home or a neighbor's property during the project, you will be solely responsible for covering the repair costs. General Liability insurance would typically cover this, but without it, the bill comes directly to you.

- Legal Battles and Stress: Uninsured incidents often lead to lengthy and expensive legal disputes. You could face lawsuits from injured workers, property owners, or even the contractor themselves if disputes arise. The emotional and financial toll of such battles can be immense.

- Project Abandonment & Substandard Work: Unlicensed and uninsured contractors are often less reputable, less experienced, and less invested in their business's long-term success. This makes them more prone to abandoning projects or performing shoddy work, leaving you with an unfinished or structurally unsound home and no recourse.

- No Warranty Protection: A licensed, insured contractor typically offers warranties on their work. An uninsured contractor has no legal or financial obligation to honor any guarantees, leaving you with no protection if issues arise post-completion.

In essence, hiring an uninsured contractor means you are assuming all the risks of the project, transforming your home into their personal insurance policy. This is a gamble no California homeowner should ever take.

How to Verify a Contractor's Insurance & Licenses in California

Empowering yourself with the knowledge to verify a contractor's credentials is your best defense. Don't just take their word for it; perform due diligence before signing any contract.

1. Request Certificates of Insurance (COI)

Always ask your prospective contractor for current Certificates of Insurance (COI) for General Liability and Workers' Compensation. A COI is a standard document issued by an insurance company that summarizes the contractor's coverage. What to look for on a COI:

- Policy Numbers: Ensure they are legitimate.

- Effective Dates: Verify the policies are current and will cover the entire duration of your project.

- Coverage Limits: Check that the limits are adequate (e.g., $1M for General Liability).

- Contractor's Name: Ensure it matches the name on their license and contract.

- Insurance Company: Note the name of the insurer.

2. Direct Verification with the Insurer

The most important step: contact the insurance company directly using the information on the COI. Ask them to verify the policy's validity and coverage limits for the specific contractor. Fraudulent COIs exist, so direct verification is essential.

3. Check the CSLB Website

The California Contractors State License Board (CSLB) provides an invaluable online tool for homeowners. Visit cslb.ca.gov and use their "Check a License" search tool.

- License Status: Confirm the license is active and in good standing.

- Bond Information: Verify the contractor's bond is current.

- Workers' Compensation: The CSLB website will clearly state if the contractor has Workers' Comp insurance or if they are exempt (meaning they have no employees). If they claim to have employees but the CSLB shows an exemption, that's a major red flag.

- Contractor Information: Ensure the name and address match the information provided by the contractor.

- Disciplinary Actions: The CSLB site also reveals any past disciplinary actions or consumer complaints.

4. Additional Due Diligence

- References: Ask for and contact several recent references. Inquire about their experience, project completion, and any issues that arose.

- Written Contracts: Always insist on a detailed, written contract that outlines the scope of work, timeline, payment schedule, and proof of insurance requirements.

- Never Pay in Full Upfront: California law limits down payments for home improvement projects to 10% of the contract price or $1,000, whichever is less.

Powercore Inc: Your Fully Licensed, Insured, and Trusted California Partner

At Powercore Inc, we understand that trust is the foundation of any successful home improvement project. As a leading dual-licensed General B (#1134334) and C-10 Electrical Contractor (#1098175) based in Roseville, CA, and serving all of California, we proudly stand by our commitment to transparency, professionalism, and comprehensive client protection.

Our extensive range of services – including solar installation, battery storage, HVAC solutions, roofing, ADU construction, remodels, EV charging installation, siding, decking, and interior remodeling – are all backed by our unwavering dedication to exceeding California's stringent licensing and insurance requirements. We ensure that every project we undertake is fully covered by the necessary General Liability and Workers' Compensation insurance, providing you with the ultimate peace of mind.

When you choose Powercore Inc, you're not just hiring a contractor; you're partnering with a team that prioritizes your safety, your investment, and the successful, worry-free completion of your vision. Our comprehensive coverage isn't just a legal formality; it's a testament to our integrity and commitment to delivering exceptional service without exposing you to unnecessary risks.

Conclusion: Build with Confidence, Not Concern

Embarking on a home improvement journey in California should be an exciting and rewarding experience, not a source of anxiety. By understanding and diligently verifying contractor insurance requirements, you empower yourself to select a reputable, responsible, and financially secure partner for your project.

Never underestimate the protective power of proper insurance. It's the silent guardian against unforeseen accidents, costly liabilities, and potential financial ruin. Insist on seeing current Certificates of Insurance and confirm details directly with the CSLB and the insurers. Your due diligence is the cornerstone of a successful, stress-free home transformation.

Ready to start your next California home project with complete confidence and peace of mind? Contact Powercore Inc today for a consultation. Our expert team is ready to discuss your vision and demonstrate our commitment to safety, quality, and your complete satisfaction. Call us at 916-699-8778 and let’s build your dreams, securely.